Pole Barn Financing Is More Accessible Than You Think

April 8, 2026

Most people assume financing a pole barn is complicated, niche, or simply not possible through a regular lender. In many cases, that assumption is wrong, and it stops buyers from moving forward with projects that are fully fundable. Pole barn financing and investment planning is a well-established category with multiple loan pathways, including government-backed programs. Unfortunately, many buyers never think to ask about other financing options.

Yes, You Can Finance a Pole Barn

Banks and lenders can and do accept pole barn loan applications. Post-frame buildings, the technical term for pole barn construction, can qualify for financing because lenders evaluate structural permanence and appraised value rather than the construction method itself. A pole barn built on a permanent foundation on land you own is treated as a real property improvement, which opens the door to multiple loan products. In the simplest of terms, pole barns are built for long-term use, so they can qualify for financing.

The confusion over financing options mostly comes from how people think about mortgages. Traditional home loan language doesn't describe pole barns well, leading buyers to assume those loans don't apply to them. In most cases, the right loan is simply a different product than a standard home mortgage, and the options are more accessible than you'd expect.

Why Many Buyers Assume It Is Impossible

The assumption that pole barns can't be financed has a real origin. Early lenders lacked consistent appraisal frameworks for non-traditional structures, so some applications were declined simply because underwriters didn't know how to evaluate the collateral. That gap has largely closed. Modern lenders, especially those serving rural and agricultural markets, have adapted their underwriting to accommodate post-frame buildings.

There's also a language problem. Searching for a "pole barn mortgage" on a bank's website returns nothing, not because the product doesn't exist, but because the loan lives under a different name. Construction loans, agricultural loans, and rural development programs all cover pole barns. You have to know which category fits your project.

Programs That Specifically Cover Pole Barns

Several well-known government programs recognize pole barns as eligible structures. The USDA Farm Service Agency offers Farm Ownership Loans and the Farm Storage Facility Loan program for qualifying agricultural structures, with rates that have historically ranged from 1.375% to 3.75%. USDA Rural Development programs cover rural outbuildings and barndominium-style builds in eligible areas. Farm Credit Services provides agricultural construction loans designed specifically for farm infrastructure. FHA Title I loans can fund smaller pole barn projects tied to an existing property.

These programs exist specifically for buyers in rural and agricultural settings. If you own land in an eligible area, at least one of these is likely to fit your situation.

Key Takeaway: Pole barn financing is not a workaround. It is a recognized lending category supported by USDA programs, agricultural lenders, and construction loan products. Most buyers qualify through at least one pathway once they understand which loan type fits their project.

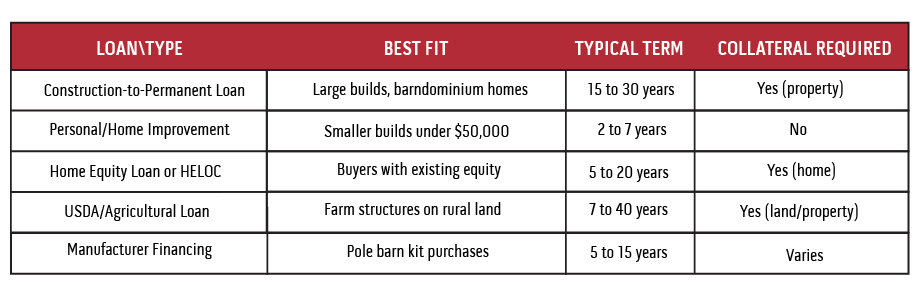

Loan Options for Pole Barn Financing

Understanding which loan category fits your project is the single most important step before you contact any lender. There are five main paths, and choosing the wrong one up front wastes time and can lead to unnecessary denials.

Construction Loans vs. Personal Loans vs. Ag Loans

A construction loan is a short-term, draw-based loan that releases funds in stages as your pole barn is built. At project completion, it typically converts into a permanent mortgage or is paid off. Construction loans are the best fit for large builds where the structure will be appraised as a permanent improvement. They require more documentation and take longer to close, but they offer better rates than unsecured products.

A personal loan or home improvement loan is unsecured, meaning no collateral is required. Approval is faster, sometimes within a few days, but interest rates are significantly higher. Personal loans work well for smaller pole barn projects in the $10,000 to $50,000 range, where speed matters more than rate optimization.

Agricultural loans, including those through the USDA Farm Service Agency and Farm Credit Services, are purpose-built for farm and rural structures. These carry the most competitive rates of any category and are the right choice for buyers whose pole barn will serve an agricultural purpose on rural land.

Will a Barndominium Change Your Loan Type?

A pole barn intended as a primary residence, commonly called a barndominium, is treated very differently than a storage or agricultural structure by most lenders. Traditional mortgage lenders often decline barndominium applications because standard appraisal comparables don't exist in many markets. That gap has created a category of specialized barndominium lenders who now exist specifically to fill it.

Regional agricultural banks and Farm Credit institutions offer construction-to-permanent loans for barndominium builds. A construction-to-permanent loan converts a short-term build loan into a standard long-term mortgage at project completion, which means only one closing and one set of fees. If your pole barn will have living space, utilities, and meet local habitability codes, this is the loan category to research first.

Q: Can I use a regular mortgage to finance a pole barn home?

A conventional mortgage from a traditional lender is unlikely to work for a barndominium because most lenders require comparable sales data for appraisal, and barndominiums lack that data in many markets. Specialized barndominium lenders and agricultural banks fill this gap with construction-to-permanent loan products designed for post-frame residential builds. FHA loans can also apply if the structure meets habitability and local code requirements.

Typical Pole Barn Loan Rates and Terms

Rates vary significantly depending on the loan type you use, and the differences are not small.

That spread matters in real dollars. On a $50,000 pole barn loan over 10 years, choosing a personal loan at 18% over a USDA program at 5% could cost you more than $15,000 in additional interest. The right loan type is worth the extra effort to find.

For post-frame construction, basic pole barn builds cost approximately $15 to $40 per square foot for utilitarian storage structures. Finished barndominium-style builds run $45 to $100 per square foot. That compares to $100 to $200 per square foot for stick-frame construction at equivalent sizes, according to cost data from the National Frame Building Association. That cost advantage is one reason pole barn financing often produces a stronger return on investment than financing a traditional garage of the same square footage.

Loan terms depend heavily on the product. Personal loans can typically be capped at 7 years. Home equity loans run 5 to 20 years. USDA agricultural loans can extend to 40 years for major farm infrastructure. Construction-to-permanent loans for barndominium homes follow standard mortgage timelines of 15 to 30 years.

Pro Tip: Before applying anywhere, get at least one written quote from a licensed pole barn builder. Lenders prefer detailed cost breakdowns over rough estimates when calculating loan-to-value ratios, and a formal quote can strengthen your application and prevent mid-project financing surprises.

Pole Barn Investment Value and ROI

A pole barn rarely returns dollar-for-dollar at resale the way a kitchen renovation might. But the ROI calculation for a pole barn is better understood through two separate lenses: immediate utility value and long-term property appeal. When you account for both, the investment picture looks quite different than a simple cost-versus-sale-price comparison.

A pole barn that eliminates $3,000 per year in off-site equipment storage costs pays back that expense within a few years, regardless of what it does to the appraised value. If it also generates rental income from farm equipment storage, a workshop lease, or hay storage, the monthly cash flow can service the loan entirely and turn net positive.

How Pole Barns Compare to Garage Additions

Post-frame pole barn construction costs 30% to 50% less per square foot than stick-frame garage construction at comparable sizes, according to contractor cost data compiled by Angi and regional builder quotes.

The appraised value contribution of both structures is typically evaluated using the cost approach, meaning appraisers assess the depreciated replacement value of the structure rather than comparing it to similar sales. A well-maintained pole barn in good condition with electrical service and insulation will appraise higher than a deteriorating structure of the same size. Condition management matters more in outbuilding appraisals than in home interiors.

Zoning considerations also differ. Pole barns in agriculturally zoned areas typically face fewer permitting restrictions than attached garages in residential zones, which can significantly reduce project costs and timelines.

Resale Value in Rural vs. Suburban Markets

When talking about the most important thing in real estate, the old adage is “Location, location, location.” Not surprisingly, it applies here.

Location changes the investment math dramatically. In rural and agricultural markets, a large functional pole barn is often listed as a premium feature in property listings and genuinely increases buyer demand. Research from land-grant university extension programs, including studies from Iowa State University Extension and Purdue Extension rural property specialists, suggests that a well-built 40x60 or larger barn on rural land can increase appraised property value by $15,000 to $50,000 depending on region, condition, and local market demand, with functional agricultural barns in farm-belt states recovering 50% to 80% of construction cost in appraised value.

Suburban markets are more variable. A pole barn on a two-acre suburban property may appeal to some buyers and deter others. In those markets, a detached garage or workshop finish reliably increases broad appeal among buyers more than a large agricultural-style structure.

Key Takeaway: Pole barn ROI is strongest when the structure serves an active function, whether for agricultural use, equipment storage, or rental income. In rural markets, a well-maintained barn frequently increases buyer demand and asking price. In suburban markets, finish level and visible utility matter more.

How the Pole Barn Loan Approval Process Works

The approval process for a pole barn loan follows a predictable sequence. Most buyers who understand the steps in advance move through them faster and avoid the two most common causes of delay: incomplete documentation and choosing the wrong loan type upfront.

Here is the sequence most construction and agricultural loan applications follow:

- Step 1: Choose the right loan type. Match your project to the correct loan category using the table above. A storage barn on farmland connects to agricultural programs. A barndominium connects to construction-to-permanent lenders. Getting this right before you apply prevents a mismatch denial.

- Step 2: Complete pre-qualification. Contact two or three lenders in your target category and complete pre-qualification with each. This typically involves a soft credit check, a basic review of income and debt, and a description of the project. Pre-qualification takes 1 to 3 business days at most lenders.

- Step 3: Gather documentation. Lenders will request proof of land ownership or a property survey, contractor bids with itemized cost breakdowns, your last two years of tax returns, current pay stubs or business financial statements, and a description of the structure's intended use.

- Step 4: Appraisal and underwriting. For construction loans, lenders typically order an as-completed appraisal, which estimates the structure's value after construction is finished rather than appraising the current state of the land. Underwriting reviews your debt-to-income ratio, credit profile, and appraisal together to make the final lending decision.

- Step 5: Closing and first draw. After approval, closing typically takes about one week. Construction draw funds are released in stages tied to verified project milestones, such as foundation completion, framing, and roof installation.

What Lenders Look For in Pole Barn Loans

- Credit score: Personal loans typically require a minimum score of 600-640. Home equity loans and construction loans generally require a credit score of 660 or higher. USDA and agricultural loans vary, but often work with scores as low as 640 for qualified rural borrowers.

- Land ownership: Most construction and agricultural loans require that you own or are purchasing the land where the barn will be built. Leased land complicates collateral and reduces the range of available loan products significantly.

- Down payment: Construction loans often require 10% to 20% down. Agricultural loans through USDA programs can require as little as 5% for qualifying borrowers.

- Debt-to-income ratio: Most lenders want total monthly debt obligations, including the projected barn payment, to stay below 43% of gross monthly income.

- Permits and plans: Some lenders require building permits or engineered plans at the time of application, particularly for construction loans. Having these ready in advance speeds up underwriting.

Typical Timeline from Application to First Draw

A realistic timeline for a pole barn construction loan looks like this, based on industry averages from lender processing data:

- Pre-approval: 1 to 2 weeks

- Appraisal and underwriting: 2 to 4 weeks

- Closing: approximately 1 week

- First construction draw: released after the first verified project milestone, typically within 1 to 2 weeks of construction start

[Source: Bankrate construction loan guide, 2024]

Total time from application to first draw typically runs 5 to 8 weeks for a construction loan. Personal loans move significantly faster, with approvals in 1 to 5 business days for qualified borrowers.

Q: What is the minimum credit score needed to finance a pole barn?

The minimum credit score depends on the loan type. Personal loans are available with scores starting around 600, though rates will be higher at the lower end. Construction loans and home equity products typically require a score of 660 or higher. USDA agricultural programs can often work with scores as low as 640 for rural borrowers who meet income and land eligibility requirements. Borrowers with scores below 600 should consider improving their credit before applying, or explore whether a co-borrower with stronger credit could strengthen the application.

Pole barn financing is genuinely accessible once you understand which product fits your project. The buyers who succeed are the ones who match their loan type to their purpose before they start talking to lenders, gather complete documentation upfront, and treat the pre-approval step as the starting line rather than an obstacle. The process is predictable, the programs are real, and for most rural and agricultural property owners, at least one of these pathways leads to an approved loan.

Contact Matador to discuss your pole barn project -- while we can't give financial advice, we can offer suggestions to help you determine the financing option that works best for you!

Frequently Asked Questions About Pole Barn Financing

Can you get a loan for a pole barn?

Yes. Pole barns and post-frame buildings qualify for several loan products, including construction loans, home equity loans, USDA agricultural programs, and manufacturer financing. Lenders evaluate structural permanence and appraised value rather than construction method, so a pole barn built on a permanent foundation on land you own is treated as a real property improvement and opens the door to multiple financing options.

What credit score do you need to finance a pole barn?

It depends on the loan type. Personal loans are available with scores starting around 600, though rates will be higher at the lower end. Construction loans and home equity products typically require a score of 660 or higher. USDA agricultural programs often work with scores as low as 640 for rural borrowers who meet income and land eligibility requirements. Borrowers with scores below 600 should consider improving their credit first or explore whether a co-borrower could strengthen the application.

What is the best loan for a pole barn?

The best loan depends on your project's purpose, size, and location. Agricultural loans through the USDA Farm Service Agency or Farm Credit Services offer the most competitive rates for farm structures on rural land. Construction-to-permanent loans are the strongest fit for large builds and barndominium-style homes. Home equity loans work well for buyers with existing equity who want predictable fixed payments. Personal loans are best reserved for smaller projects under $50,000 where speed matters more than rate.

Can you finance a barndominium with a regular mortgage?

A conventional mortgage from a traditional lender is unlikely to work for a barndominium because most lenders require comparable sales data for appraisal, and barndominiums lack that data in many markets. Specialized barndominium lenders and agricultural banks offer construction-to-permanent loan products specifically designed for post-frame residential builds. FHA loans can also apply if the structure meets local habitability and building code requirements.

Do pole barns increase property value?

In rural and agricultural markets, a well-built pole barn can meaningfully increase property value and buyer demand. Research from Iowa State University Extension and Purdue Extension suggests a well-maintained 40x60 or larger barn on rural land can increase appraised property value by $15,000 to $50,000, depending on region, condition, and local market demand, with functional agricultural barns in farm-belt states recovering 50% to 80% of construction cost in appraised value. Results in suburban markets are more variable and depend heavily on finish level and visible utility.

How long does it take to get a pole barn loan approved?

Construction loans typically take 5 to 8 weeks from application to first draw, including 1 to 2 weeks for pre-approval, 2 to 4 weeks for appraisal and underwriting, and approximately 1 week for closing. Personal loans are processed much faster, with approvals available in 1 to 5 business days for qualified borrowers. Having complete documentation ready before you apply — including land ownership records, contractor bids, and tax returns — is the single most reliable way to shorten the timeline.

Does the USDA offer pole barn financing?

Yes. The USDA Farm Service Agency offers Farm Ownership Loans and the Farm Storage Facility Loan program for qualifying agricultural structures. USDA Rural Development programs also cover rural outbuildings and barndominium-style builds in eligible areas. Rates on USDA agricultural programs have historically been among the most competitive available for rural construction, and some programs require as little as 5% down for qualifying borrowers. Eligibility depends on property location, intended agricultural use, and income qualifications.

What do lenders look for when approving pole barn financing?

Lenders evaluate credit score, land ownership, down payment, debt-to-income ratio, and the intended use of the structure. Most construction and agricultural loans require that you own or are purchasing the land where the barn will be built. Lenders typically want total monthly debt obligations to stay below 43% of gross monthly income. Having engineered building plans, a building permit, and an itemized contractor bid ready before you apply strengthens your application and speeds up underwriting.

The information in this article is provided for general educational purposes only and does not constitute financial, lending, or legal advice. Loan program availability, interest rates, credit requirements, and eligibility criteria vary by lender, state, and individual borrower circumstances and are subject to change without notice. USDA program details, tax treatment, and appraisal outcomes depend on factors specific to your property and financial situation. Always consult with a licensed lending professional, financial advisor, and qualified tax professional before making any financing decisions related to pole barn construction or rural property improvement.